>ACADEMY INSTRUMENTS

CAP FLOOR

Container Option setting the reference rate, fixed or floating, above (cap) or below (floor) which the buyer / holder receives payments, calculated based on cap rate or floor rate and a notional.

Container, because, usually, many reference periods (for payments) are addressed, and each reference period is a caplet or floorlet and has, among other things, a payment date associated with it. And in case the reference rate is floating, usually 3 or 6 months, each caplet or floorlet also has a fixing date.

Understandably, each caplet is a European call option, and each floorlet is a European put option.

\[\scriptsize{\textsf{Payoff}}_{caplet}={\textsf{nominal}}\,\cdot\,{\textsf{dayCountFraction}}\,\cdot\,max({\textsf{referenceRate}} - {\textsf{strike}}, 0)\] |

\[\scriptsize{\textsf{Payoff}}_{floorlet}={\textsf{nominal}}\,\cdot\,{\textsf{dayCountFraction}}\,\cdot\,max({\textsf{strike}} - {\textsf{referenceRate}}, 0)\] |

FORWARD RATE AGREEMENT

If you agree over-the-counter (OTC) to an interest rate in the future (forward rate), add a (floating) market rate as reference (relevant for settlement), and base it on a notional amount (relevant for settlement), and agree to settle in cash an amount equal to the difference between forward rate and reference rate, applied to the notional, then you have a forward rate agreement (FRA).

So, there is a fixed rate involved, as well as a floating rate.

The party paying the fixed rate is the borrower. The other party paying the difference of fixed to floating is the lender.

Settlement occurs when the floating rate is fixed, that is, at the beginning of a period. Therefore, the due payment is discounted back to the beginning of a period.

INTEREST RATE FUTURE

Underlying is an interest rate paying instrument, and therefore it gives exposure to changes in interest rates.

The exposure is firstly in its price or value, and secondly in terms of the interest rate of the underlying.

Short- term interest rate (STIR) futures have (often) a 3-month interest rate security as underlying.

Long-term interest rate futures are bond futures.

TODO

BOND

Two ways to quote a bond's price:

- Dollar value

- Yield

Primary market

Secondary market

TODO

BOND FUTURE

TODO

INTEREST RATE SWAP

TODO

SWAPTION

TODO

REPO

TODO

OPTION

Based on [1] and [3].

From a retailer's perspective, options can be considered directional instruments.

But pricing and hedging of options can be understood when considering the interbank perspective of market maker / dealer, in which options are instruments of volatility.

That is, for a retail investor owning a call option on an asset, a consistent upward move in the underlying may be perceived as good.

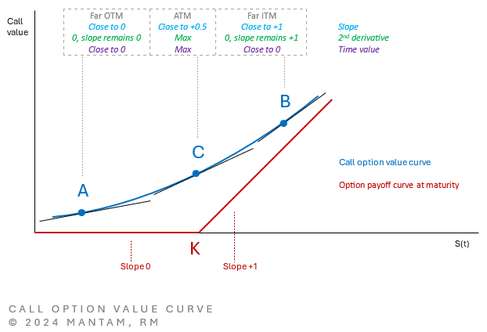

But a market maker owning the same call option may well prefer that the underlying price oscillates as much and as often as possible, and the more this happens, the more a long position (in a call or a put) will gain, and a short position (in a call or a put) will lose. This is so, because of the options gamma, the second derivative, and if it happens when the option is at-the-money, the gains of a long call or put position, and the losses of a short call or put, are maximized, given that gamma is maximized. The diagram below shows this.

Quote from an unknown source in [3]: "...the big potential profit from these trades is from gamma, in other words, large moves in the underlying rather than changes in implied vol."

Convexity of option value curve, volatility, cash earnings

Option value curve C(t) or \(C(S_t,t)\].

With everything else being the same, the greater the curvature of C(t), the greater the time value. A greater curvature means that the option premium will change more with a change in S(t). Refer to >Black-Scholes PDE for details on cash earnings.

Interest rate options

- Caps, floors, collars

- Swaptions

- Cancelable and extendible swaps

- Compound options

- Exotic options

- Embedded options

Exotic options

- Path-dependent: barrier, asian, lookback, cliquet, ladder

- Time-dependent: chooser, delayed or forward-starting

- Digital

- Multi-variate: rainbow, basket, spread, quanto

Option pricing models, such as Black-Scholes, assume that market prices of the underlying follow a random walk. However, because interest rates don't have this behavior of ever expanding, but rather periodically return and have a more confined range of values (for example, usually not exceeding, say, 10%), other models are better for pricing their options.

Note on pricing options vs linear derivatives and securities

For securities (such as bonds) and non-option derivatives (these are linear derivatives, such as FRA, forward, swap), the pricing is possible via construction of a static and riskless hedge to determine a fair price. This is so, because two things are given at maturity:

(a) a rigid relationship between the price of the derivative and prices of the underlying, and

(b) a definite procedure that takes place upon maturity.

For options, (a) is also given, but not (b).

That is, it's unclear whether the option will be exercised or not. This lack of certainty as to what will eventually happen on the maturity date makes options different compared to linear derivatives.

An option buyer has the right to decide later whether to exercise the option or not, and the time-value of the option is the value of this right.

Option pricing

Various approaches:

- Closed-form solution, such as the closed-form Black-Scholes formula (which is derived by applying a series of assumptions to the Black-Scholes model)

- Binomial model

- Monte Carlo simulation

- Finite Difference method

No matter which, the same five inputs are needed:

- Underlying asset price

- Strike price

- Time to option expiry

- Carry (combination of interest rates and potential earnings on the underlying)

- Volatility

Volatility is the only input that is not readily available. The others are either set in the contract, or observed in the market.

Option types

- European: option holder can exercise at maturity only

- Bermudan: at maturity, and at least one more date prior to that

- American: any time up to maturity

How to view a European option

Based on [2, p29].

| TYPE | BETTER | CONVENTIONAL |

| CALL | Asset with payoff (S−K)+ at future time T. | The right to buy asset at price K at future time T. |

| PUT | Asset with payoff (K−S)+ at future time T. | The right to sell asset at price K at future time T. |